#161 Amortized Inference & Neural Processes, with Luigi Acerbi

Jul 16, 2026 - 01:32:14

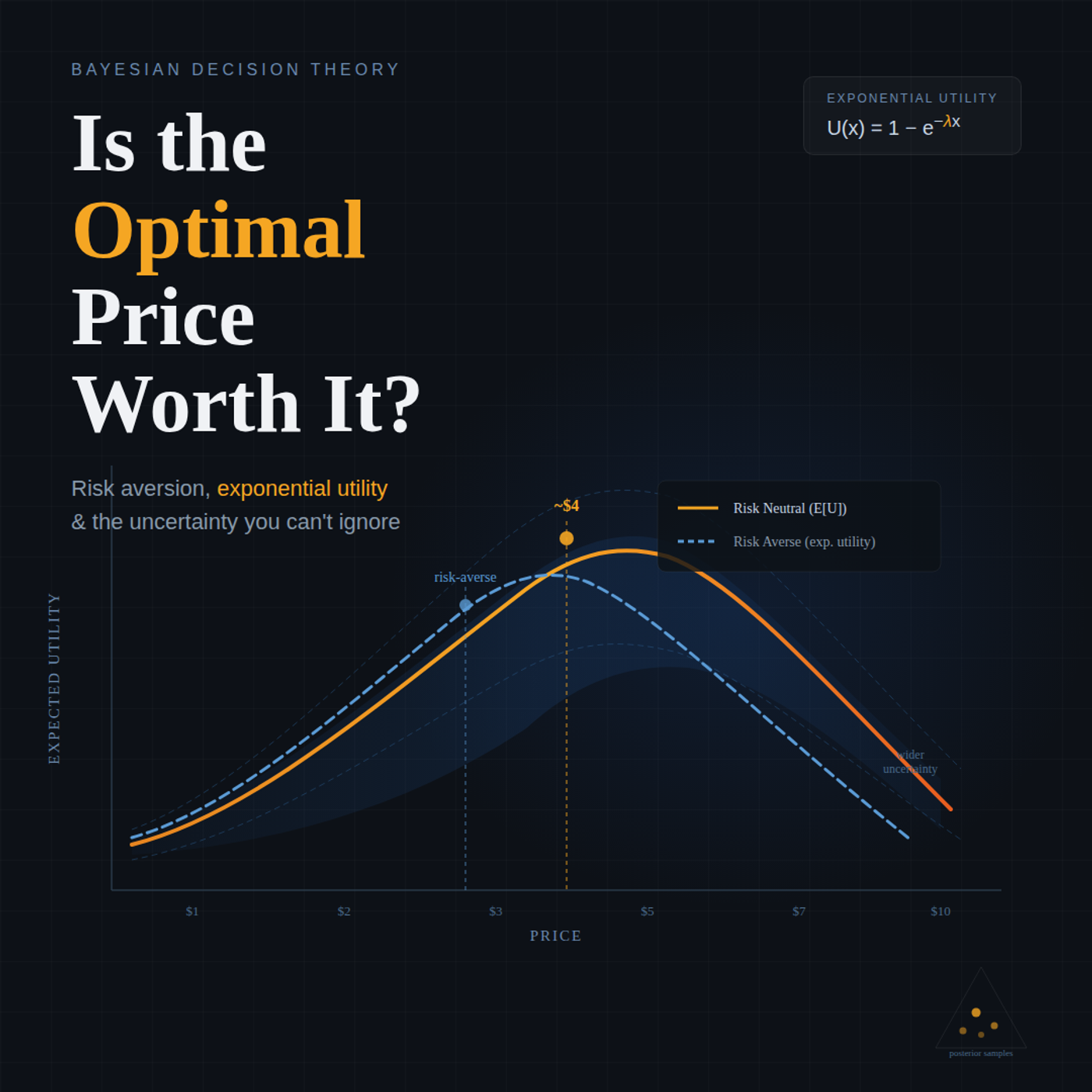

Today's clip is from Episode 152 of the podcast, featuring Daniel Saunders. In this conversation, Daniel explores how Bayesian decision theory handles real-world risk aversion beyond the textbook maximum expected utility...

Pricing Under Uncertainty: A Bayesian Workflow is an episode from Learning Bayesian Statistics by Alexandre ANDORRA. Today's clip is from Episode 152 of the podcast, featuring Daniel Saunders. In this conversation, Daniel explores how Bayes...

This episode belongs to Learning Bayesian Statistics.

Use the player on this page to stream the episode online.

Published Apr 16, 2026, 00:05:03 long, audio available.

Continue listening to more episodes from Learning Bayesian Statistics.

Jul 16, 2026 - 01:32:14

Jun 29, 2026 - 01:40:31

Jun 19, 2026 - 00:04:46

Jun 10, 2026 - 00:04:25

Jun 8, 2026 - 01:26:06

Jun 2, 2026 - 00:04:50

May 21, 2026 - 01:18:31

May 13, 2026 - 00:03:57